By Julie Bech, co-Portfolio Manager of Nordea – 1 Global Diversity Engagement Fund

To date, the ‘E’ has dominated focus within the ‘ESG’ landscape, with environmental concerns like climate change high on the list of investor priorities, while the ‘S’ has lagged. But with projected investments in Diversity & Inclusion set to reach USD 15 bn by 20261, we’re starting to see a subtle but notable shift. More and more companies are recognizing the real value a diverse corporate culture can add, from employee retention to broader client and consumer bases, among other things. Positive diversity practices often translate into a material impact on companies’ financial performances and shareholder values—which is good news for investors.Diverse companies perform better

There is growing research confirming that companies with stronger diversity and inclusion have a competitive advantage over their peers. For example, The Harvard Business Review published an article2 highlighting numerous studies that show large cap companies with at least one woman on their board generated a higher return on equity (a measure of profitability) and net income growth (the rate of profit growth) compared to those companies that had no gender diversity. A McKinsey study of more than 1,000 companies further supports this finding; it reported that those in the top quartile of gender diverse executive teams were 25% more likely to outperform on profitability, while those in the bottom quartile were 27% less likely to experience profitability above the industry average.3Diversity can bear fruit

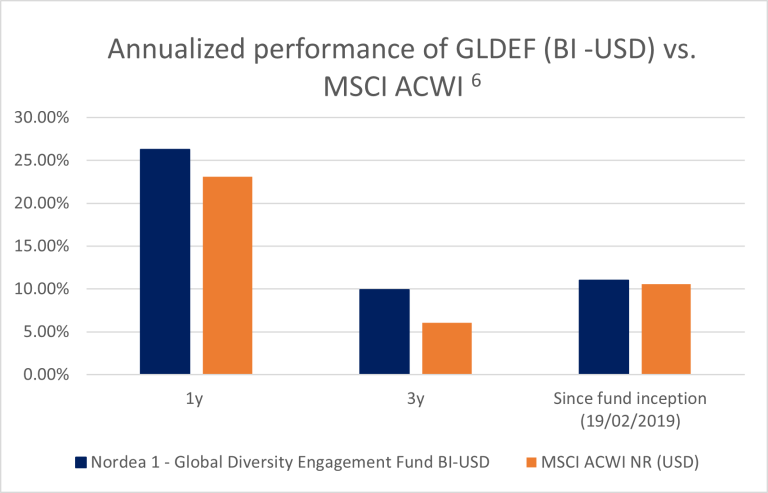

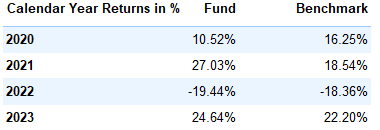

In our view, the logical knock on effect of better performing companies is better performing investments in those companies. An increasing body of data demonstrates there is a link between corporate social responsibility and financial performance4yet the investment trend behind it is just getting started. We believe that active managers with the right analytics and engagement tools can leverage the investment gap that currently exists, to deliver returns and responsibility. Hence, we were an early mover in this space in 2019 when we launched Nordea 1 – Global Diversity Engagement Fund. The five star Morningstar solution5 builds on broad research confirming that companies with stronger diversity and inclusion have a competitive advantage over their peers. The Fund (BI USD) has returned 69% since inception, outperforming the benchmark by 3.4%6, demonstrating the success of an active management approach within this theme and also supports the academic research on corporate diversity. See chart below.

We engage for change

Nordea 1 – Global Diversity Engagement Fund focuses on D&I as drivers for social change, while also taking advantage of the positive correlation between above average D&I practices and corporate financial performance. We believe that one of the best ways to achieve a more diverse corporate environment that offers equal opportunities to all is by engaging with companies and supporting them in a well-defined path towards D&I excellence.

As such, our portfolio consists of leaders, improvers and moderate laggards in terms of D&I policies and practices. Our engagement efforts are focused on the latter two groups, where most stakeholder interaction is needed. Drawing upon the extensive expertise of NAM’s Responsible Investments (RI) team—one of the most experienced of its kind in Europe—we help companies make positive changes that can have a big impact on their bottom line.

The focus on diversity has gained significant traction because in addition to being a worthy social cause, it has genuine economic merit. Ensuring that more diverse people are working and leading in the workplace is simply good business. As demographic headwinds emerge, companies can benefit by incorporating sound D&I practices. Nordea 1 – Diversity Engagement Fund demonstrates what’s good for companies is good for investors.

1McKinsey & Company, Diversity, Equity and Inclusion Lighthouse 2023, Jan 2023

2The Harvard Business Review, Why Diverse Teams are Smarter, Nov 2016

3McKinsey & Company, Diversity wins: How inclusion matters, May 2020

4Journal of Sustainable Finance & Investment, ESG and Financial Performance: Aggregated Evidence from More than 2000 Empirical Studies’, Oct 2015.

5© 2024 Morningstar, Inc. All Rights Reserved as of 31/01/2024. The Morningstar Rating is an assessment of a fund’s past performance — based on both return and risk — which shows how similar investments compare with their competitors. A high rating alone is insufficient basis for an investment decision.

6Source: Nordea Investment Funds S.A. Period under consideration: 21.02.2019 – 29.02.2024. Performance calculated NAV to NAV (net of fees and Luxembourg taxes) in the currency of the respective share class, gross income and dividends reinvested, excluding initial and exit charges as per (29.02.2024). Initial and exit charges could affect the value of the performance. Past performance is not a reliable indicator of future results and investors may not recover the full amount invested. The value of your investment can go up and down, and you could lose some or all of your invested money.